Business Credit Scores &

Reports

Strong business credit scores can be key to getting your company approved for trade credit and financing. But they can be very different than personal credit scores. Understand how they work and how to build strong business credit.

Get your free scores

Business credit score factors in this article:

What is Business Credit Score?

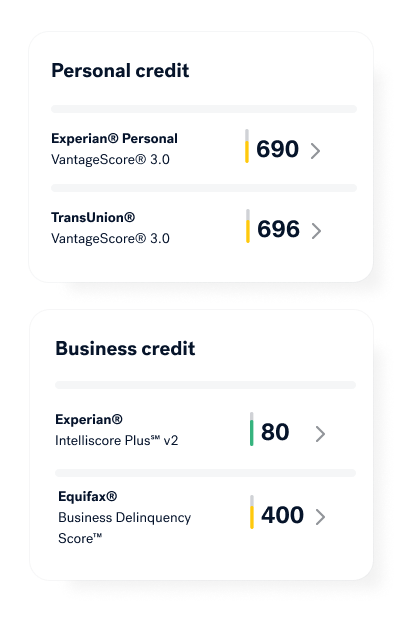

Personal credit scores rank creditworthiness of individuals, business credit scores do the same for businesses. Personal credit scores range from 300 to 850. Business credit scores range from 0 to 100. Major business credit reporting agencies Dun & Bradstreet, Experian, and Equifax produce business credit scores and reports. FICO scores for small businesses are known as “FICO SBSS.”

If you try to compare business credit to personal credit, you’re likely to get frustrated. That’s because business credit scores differ from consumer credit scores in some key ways:

Credit Score Ranges: Personal FICO scores range between 300 to 850; business credit scores typically range between zero to 100. Paying on time to lenders and/or creditors is the best thing you can do to establish a good business credit score.

Free scores: There are over 150 places where consumers can check and monitor their consumer credit scores for free. But free business credit scores are available from a very limited number of sources, such as Nav.

Access: Anyone can check a businesses’ credit scores, unlike consumer scores which are restricted to anyone with a “permissible purpose” under federal law.

Accuracy: A study published in the Wall Street Journal found as many as 25% of business credit reports may contain errors or are missing key information. If the credit report contains mistakes, the scores produced may not accurately reflect the risk of the business.

Free Personal and Business Credit Scores

See how lenders view your business data and apply for financing you’re likely to qualify for.

Sign UsBy clicking “Sign Up” below, you confirm that you accept the Terms and Conditions, acknowledge receipt of our Privacy Notice and agree to its terms.

Intelliscore Plus℠ from Experian

With the Experian Intelliscore Plus℠ scores range from 1 to 100. A Higher scores indicate lower risk, so as a business owner, you want to aim for a higher score.

There are over 800 variables that can go into these scores, including tradeline and collection information, public filings, new account activity, key financial ratios and other performance indicators. But the bottom line is paying on time and managing debt well will help build a strong score.

Note: Experian offers a version of Intelliscore Plus that can evaluate data from the owner’s personal credit report as well as business credit.

Learn more about Experian Business Credit Reports here.

FICO® LiquidCredit® Small Business Scoring Service℠

FICO’s Small Business Scoring Service (SBSS) rank-orders applicants by their likelihood of making payments on time. The score ranges from 0 to 300. The higher the score, the better. The scoring can use both personal and business credit data and other financial information. A strong history of business credit with timely payments to vendors and suppliers may help boost your SBSS score. The FICO SBSS score will be used for term loans, lines of credit, and commercial loans up to $350,000 from the Small Business Administration (SBA). The minimum score to pass the SBA’s pre-screen process is currently 140.

Learn more about Experian Business Credit Reports here.